English

English

Deutsch

Deutsch

Français

Français

Português

Português

Español

Español

Bahasa Indonesia

Bahasa Indonesia

Tiếng Việt

Tiếng Việt

日本語

日本語

한국어

한국어

中文

中文

ภาษาไทย

ภาษาไทย

العربية

العربية

Русский

Русский

💡 Forex Inter-Broker Arbitrage: Hunting for Pips

⚙️ Why Do Inefficiencies Occur? The Role of Liquidity Providers

To understand the nature of arbitrage, one must understand the structure of liquidity provision.

Liquidity Providers (LPs) are Tier-1 banks (J.P. Morgan, Deutsche Bank, Citi) that form the interbank market. Different brokers are connected to different liquidity pools, creating micro-differences in prices.

Broker Operating Models

| Broker Type | Model Description | Price Source |

|---|---|---|

| ECN/STP (A-Book) | Intermediary. Streams LP prices to the client + commission. | Pool of banks (Citi, UBS, Barclays, etc.) |

| Market Maker (B-Book) | Counterparty. Creates an "internal" market. | Proprietary algorithms + reference to interbank |

| Hybrid | Combination of A-Book and B-Book. | Mixed flow of quotes |

Source of Arbitrage: Broker A receives a quote from Citi, while Broker B receives one from Deutsche Bank. The difference in price update speed (Latency) creates an arbitrage window.

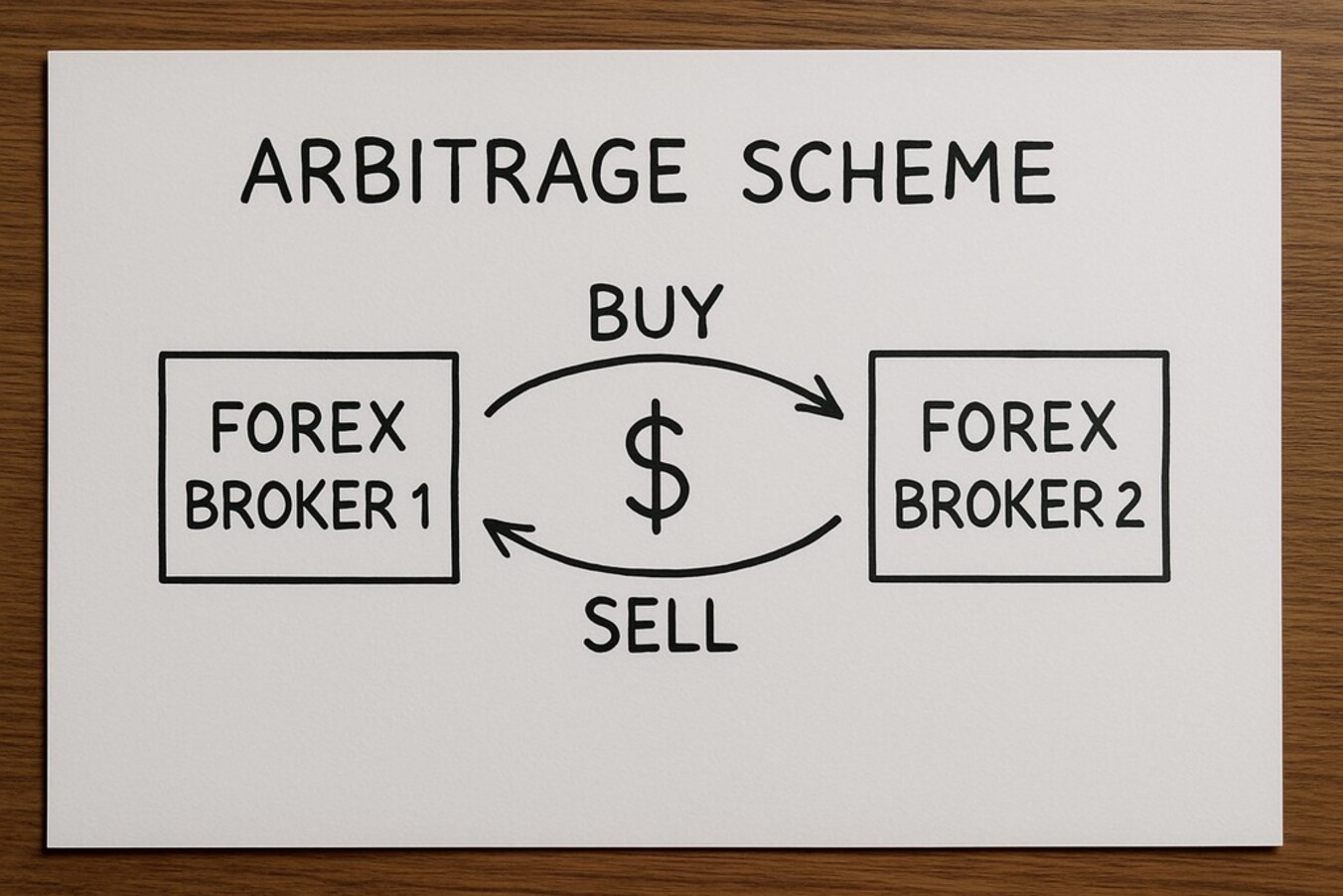

📈 Practical Case: EUR/USD Arbitrage

Step 1: Infrastructure Preparation

- Accounts: Opened with "Broker-Cheap" (ECN) and "Broker-Expensive" (Hybrid).

- Software: Specialized terminal (e.g., PairTradingPRO) or Latency Arbitrage Software.

- Hardware: VPS server in the same data center (Cross-connect) as the brokers' servers.

Step 2: Finding the Arbitrage Window (Detection)

The algorithm detects price discrepancies in real-time:

| Broker | Bid (Sell Price) | Ask (Buy Price) |

|---|---|---|

| Broker-Cheap | 1.08500 | 1.08505 (Buy here) |

| Broker-Expensive | 1.08515 (Sell here) | 1.08520 |

Signal: BidBroker2>AskBroker1 1.08515>1.08505 Difference (Spread gap) = 1 pip ($10 per 1 standard lot).

Step 3: Synchronous Execution

Within milliseconds, two orders are sent:

- BUY 1 lot EUR/USD at 1.08505 with the Cheap Broker.

- SELL 1 lot EUR/USD at 1.08515 with the Expensive Broker.

Step 4: Calculation of Mathematical Expectation

Profit is calculated using the formula:

Profitgross=Psell−Pbuy=1.08515−1.08505=0.00010 (10 points)

Profitnet=Profitgross−(CommBroker1+CommBroker2)

Where:

- Profitgross = $10

- Commissions ≈ $7 ($3.5 per lot each)

- Net Profit: 10−7=3 dollars per trade.

Arbitrage robots execute hundreds of such operations per day.

⚠️ Harsh Reality: Risks of Arbitrage

The strategy seems "risk-free" (market neutral) but carries enormous operational risks.

1. Execution Risk

The main enemy of the arbitrageur is time.

- Latency: The arbitrage window lives for 50–100 ms. If the ping is high, the price will move away.

- Slippage: The order is executed at a worse price than requested, turning profit into loss.

- Requotes: The broker refuses to execute the trade at the current price.

2. Broker Countermeasures (Toxic Flow)

Brokers (especially B-Book) classify arbitrage as "toxic flow." Countermeasures:

- Artificially widening spreads for a specific account.

- Implementing software delay (Plugin latency).

- Retroactively cancelling trades or blocking the account.

3. Technical Failures

Any desynchronization (internet outage, VPS failure) leaves the trader "legged" (with one open position), turning arbitrage into ordinary directional trading with market risk.

✅ Verdict and Requirements for Success

Manual arbitrage is impossible. It is a high-tech arms race of robots.

Checklist for a Successful Arbitrageur:

- Specialized Software: Software for HFT/Latency arbitrage.

- Co-location: VPS server in the same rack as the broker's server (London LD4, New York NY4).

- Speed: Ping < 1-5 ms.

- Broker Selection: Finding loyal ECN brokers with fast liquidity aggregation.

✍️ Article Author: JohnM

#ForexArbitrage #HFT #AlgoTrading #LiquidityProviders #LatencyArbitrage #ECN #TradingStrategy #FinTec